set.seed(1)

n <- 10 ## Dimension of matrix

m <- 1000 ## Number of samples

## Create sparse, symmetric PSD matrix S

A <- rsparsematrix(n, n, 0.15, rand.x = stats::rnorm)

Strue <- A %*% t(A) + 0.05 * diag(rep(1, n)) ## Force matrix to be strictly positive definiteSparse Inverse Covariance Estimation

Introduction

Assume we are given i.i.d. observations \(x_i \sim N(0,\Sigma)\) for \(i = 1,\ldots,m\), and the covariance matrix \(\Sigma \in {\mathbf S}_+^n\), the set of symmetric positive semidefinite matrices, has a sparse inverse \(S = \Sigma^{-1}\). Let \(Q = \frac{1}{m-1}\sum_{i=1}^m (x_i - \bar x)(x_i - \bar x)^T\) be our sample covariance. One way to estimate \(\Sigma\) is to maximize the log-likelihood with the prior knowledge that \(S\) is sparse (Friedman et al. 2008), which amounts to the optimization problem:

\[ \begin{array}{ll} \underset{S}{\mbox{maximize}} & \log\det(S) - \mbox{tr}(SQ) \\ \mbox{subject to} & S \in {\mathbf S}_+^n, \quad \sum_{i=1}^n \sum_{j=1}^n |S_{ij}| \leq \alpha. \end{array} \]

The parameter \(\alpha \geq 0\) controls the degree of sparsity. The problem is convex, so we can solve it using CVXR.

Example

We’ll create a sparse positive semi-definite matrix \(S\) using synthetic data

We can now create the covariance matrix \(R\) as the inverse of \(S\).

R <- base::solve(Strue)As test data, we sample from a multivariate normal with the fact that if \(Y \sim N(0, I)\), then \(R^{1/2}Y \sim N(0, R)\) since \(R\) is symmetric.

x_sample <- matrix(stats::rnorm(n * m), nrow = m, ncol = n) %*% t(expm::sqrtm(R))

Q <- cov(x_sample) ## Sample covariance matrixFinally, we solve our convex program for a set of \(\alpha\) values.

Positive semi-definite variables are designated using PSD = TRUE.

alphas <- c(10, 8, 6, 4, 1)

S <- Variable(c(n, n), PSD = TRUE)

obj <- Maximize(log_det(S) - matrix_trace(S %*% Q))

S.est <- lapply(alphas,

function(alpha) {

constraints <- list(sum(abs(S)) <= alpha)

## Form and solve optimization problem

prob <- Problem(obj, constraints)

result <- psolve(prob)

check_solver_status(prob)

## Create covariance matrix

R_hat <- base::solve(value(S))

Sres <- value(S)

Sres[abs(Sres) <= 1e-4] <- 0

Sres

})In the code above, the PSD = TRUE attribute restricts S to the positive semidefinite cone. In our objective, we use CVXR functions for the log-determinant and trace. The expression matrix_trace(S %*% Q) is equivalent to `sum(diag(S %*% Q))}, but the former is preferred because it is more efficient than making nested function calls.

However, a standalone atom does not exist for the determinant, so we cannot replace log_det(S) with log(det(S)) since det is undefined for a PSD variable object.

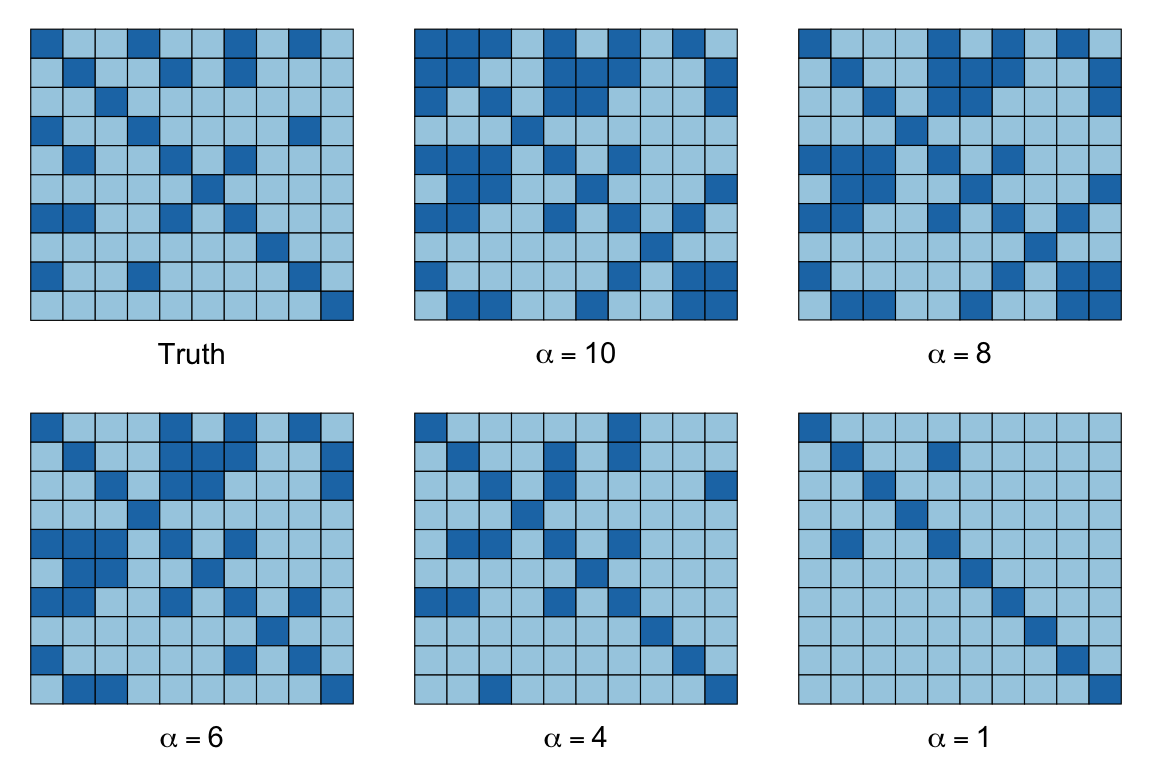

Results

The figures below depict the solutions for the above dataset with \(m = 1000, n = 10\), and \(S\) containing 26% non-zero entries, represented by the dark squares in the images below. The sparsity of our inverse covariance estimate decreases for higher \(\alpha\), so that when \(\alpha = 1\), most of the off-diagonal entries are zero, while if \(\alpha = 10\), over half the matrix is dense. At \(\alpha = 4\), we achieve the true percentage of non-zeros.

do.call(multiplot, args = c(list(plotSpMat(Strue)),

mapply(plotSpMat, S.est, alphas, SIMPLIFY = FALSE),

list(layout = matrix(1:6, nrow = 2, byrow = TRUE))))

Session Info

R version 4.6.0 (2026-04-24)

Platform: aarch64-apple-darwin23

Running under: macOS Tahoe 26.5.1

Matrix products: default

BLAS: /Library/Frameworks/R.framework/Versions/4.6/Resources/lib/libRblas.0.dylib

LAPACK: /Library/Frameworks/R.framework/Versions/4.6/Resources/lib/libRlapack.dylib; LAPACK version 3.12.1

locale:

[1] en_US.UTF-8/en_US.UTF-8/en_US.UTF-8/C/en_US.UTF-8/en_US.UTF-8

time zone: America/Los_Angeles

tzcode source: internal

attached base packages:

[1] grid stats graphics grDevices utils datasets methods

[8] base

other attached packages:

[1] expm_1.0-0 Matrix_1.7-5 ggplot2_4.0.3 CVXR_1.9.1

loaded via a namespace (and not attached):

[1] piqp_0.6.2 gtable_0.3.6 jsonlite_2.0.0 dplyr_1.2.1

[5] compiler_4.6.0 highs_1.14.0-2 tidyselect_1.2.1 Rcpp_1.1.1-1.1

[9] slam_0.1-55 cccp_0.3-3 dichromat_2.0-0.1 scales_1.4.0

[13] yaml_2.3.12 fastmap_1.2.0 clarabel_0.11.2 here_1.0.2

[17] lattice_0.22-9 R6_2.6.1 labeling_0.4.3 generics_0.1.4

[21] knitr_1.51 htmlwidgets_1.6.4 backports_1.5.1 checkmate_2.3.4

[25] tibble_3.3.1 rprojroot_2.1.1 osqp_1.0.0 pillar_1.11.1

[29] RColorBrewer_1.1-3 rlang_1.2.0 xfun_0.58 S7_0.2.2

[33] otel_0.2.0 cli_3.6.6 withr_3.0.2 magrittr_2.0.5

[37] Rglpk_0.6-5.1 digest_0.6.39 gmp_0.7-5.1 lifecycle_1.0.5

[41] ECOSolveR_0.6.1 scs_3.2.7 vctrs_0.7.3 evaluate_1.0.5

[45] glue_1.8.1 farver_2.1.2 codetools_0.2-20 rmarkdown_2.31

[49] pkgconfig_2.0.3 tools_4.6.0 htmltools_0.5.9 References

Friedman, J., T. Hastie, and R. Tibshirani. 2008. “Sparse Inverse Covariance Estimation with the Graphical Lasso.” Biostatistics 9 (3): 432–41.